Tony Nefouse’s Complete Guide to Group Insurance: Request for Proposal

At this point, you are ready to start submitting proposals for group insurance. First-year Benefit Offering: If you are offering a group health plan for the very first time, there are multiple issues to be aware of. Hopefully, you have surveyed the current employees and know who is interested in electing coverage. As the owner, […]

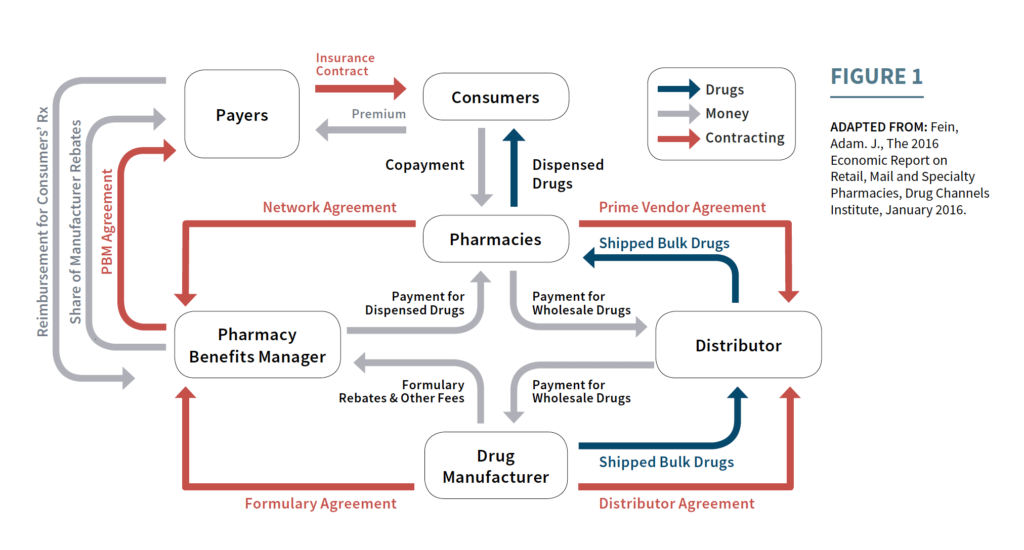

The Trumps Administration Blueprint to Lower Drug Prices

The Trump administration released the American Patient First which is a guide to lower drug prices. The blueprint provides two phases; Phase 1 is actions the President can take to lower prices, Phase 2 is for HHS actions of consideration and solicit feedback. The blueprint is looking at four areas to address, Increased Competition, Better […]

Tony Nefouse’s Complete Guide to Group Insurance: Obtaining A Quote

Obtaining proposals for group insurance benefits can be relatively easy. There are multiple outlets for receiving bids. Most of the insurance companies have now set up in-house sales; this allows groups to go direct to the carrier to obtain a proposal. Some payroll companies have broker divisions in which they can provide suggestions. The best […]

Tony Nefouse’s Complete Guide to Group Insurance

Many companies will turn to the internet to search for insurance benefits. Since 1998, we have been helping these businesses obtain group benefits. In the beginning of the internet, very few people would go to the world wide web for insurance information. Today that has all changed, business owners want information at their fingertips. We […]

Indiana Association Health Plans (AHPs)

Association Health Plan is where members can purchase health insurance that is specifically designed for that organization. At the end of 2017, President Trump issued an executive order that would allow for group of people to purchase associations health plans that are not required to cover the essential health benefits (EHBs) of the affordable […]

Pharmacy Benefit Management News

UnitedHealthcare PBM Optum is launching a new program that should have a positive impact on UHC’s fully insured membership. One of the biggest frustrations to insured individuals on health saving accounts (H.S.A) or high deductible plans, has been filling prescription drugs. On an H.S.A. plan, prescriptions will apply towards the deductible and members have seen […]

Indiana Challenging the Affordable Care Act

Indiana has joined 19 other states in a coalition to challenge the constitutionality of the Affordable Care Act (ACA). The suit was filed in federal court in Texas and is led by Texas and Wisconsin. December 2017 the tax bill was signed into law which eliminated the individual mandates financial penalties staring in 2019. […]

Employer Shared Responsibility Payment (ESRP) notification

If you are researching this topic, then you may have received a letter from the Department of Treasury Internal Revenue Service with regards to Employer Shared Responsibility Payment (ESRP). Under the Affordable Care Act’s employer shared responsibility provisions, large companies are required to offer affordable health insurance coverage that meets the requirements of the ACA. This rule is […]

Amazon, Berkshire Hathaway & JPMorgan Healthcare Transformation

There have been huge shockwaves caused in the health care industry with news that Amazon, Berkshire Hathaway & JPMorgan would form an independent health care company for their employees in the United States. Upon the release of this news, publicly traded health care companies saw their stocks prices drop as the news of new competition […]

Cadillac Tax Postponed Until 2022

Outside of open enrollment there has been little news on the Affordable Care Act. On January 22nd it was announced that the Cadillac Tax will be postponed until 2022. The postponement was included in the short-term budget bill that was signed by the president. This is a huge relief for Indiana and the rest of […]